Rule 4 Non-Runners and Box Bets: CSF Deduction Tables

Table of Contents

- Financial Impact of Non-Runners on Permutated Slips

- Rule 4 and the forecast – what gets deducted and why

- What happens to a combination forecast when one of your selections withdraws

- The Tote treatment – pool recalculation when a horse withdraws

- Getting your refund right – what the operator should put back on your card

Financial Impact of Non-Runners on Permutated Slips

Twice in the past year I’ve seen punters at the racecourse argue with cashiers about Rule 4 deductions on combination forecasts. Both arguments were lost. Both punters left convinced they’d been robbed. They hadn’t been. They’d just never read the rule that governs what happens to a perm when one of the field withdraws between off-time and the start of the race.

Steve Lewis Hamilton’s observation that «the handicap rating given to any horse is somebody’s opinion» – true as it is – is matched by an equally important truth at the slip end: the rules governing settlement of your boxed forecast or tricast are also somebody’s framework, in this case Tattersalls Committee’s Rule 4. Knowing how that framework applies to combination bets specifically is the difference between collecting what you’re owed and leaving money behind because you didn’t know to ask.

Rule 4 and the forecast – what gets deducted and why

Rule 4 in its general form is a deduction from winnings to compensate for the withdrawal of a horse after final declarations but before the race goes off. The deduction is set by the SP of the withdrawn horse – short-priced withdrawals trigger larger deductions, long-priced withdrawals trigger smaller ones. The Tattersalls scale ranges from no deduction at all (withdrawn horse at 14/1 or longer) to 90p in the pound (withdrawn horse at 1/9 or shorter favourite).

On a forecast – CSF or Tote Exacta – the application is mechanical. The CSF formula is run using the post-withdrawal SPs of the remaining runners. The starting prices of horses still in the race are themselves adjusted upward to reflect the absence of the withdrawn horse, which means the algorithm is already working off a corrected market. The published CSF dividend on a forecast involving a Rule 4 race incorporates the corrected SPs at the formula’s input level.

The published CSF on the day comes out slightly different than it would have without the withdrawal – typically lower if the withdrawn horse was a short-priced favourite (because the remaining horses’ SPs shorten to absorb that market share), and effectively unchanged if the withdrawn horse was 14/1 or longer. There’s no separate «Rule 4 deduction» applied to the CSF dividend after the fact – the deduction is baked into the formula’s inputs.

What happens to a combination forecast when one of your selections withdraws

This is where the most common confusion arises. Imagine you’ve placed a £1 combination forecast on three horses – A, B, C – for a total outlay of £6 across six possible orderings. The morning of the race, horse B is withdrawn under Rule 4. What happens to your slip?

The four orderings that involve horse B (A-B, B-A, B-C, C-B) become void. Each of those four lines is refunded to you. Your remaining live bet is the two orderings that don’t include horse B – A-C and C-A – for a total live stake of £2. The £4 covering the voided lines is refunded automatically by the operator.

If horse A and horse C then finish first and second in either order, your remaining £2 of live stake collects the CSF dividend on whichever order they finished. The dividend on the live lines is calculated using the post-withdrawal SPs of the remaining runners, as per the standard CSF mechanics described above. There’s no additional Rule 4 deduction applied to your dividend at this stage – the deduction was already in the SPs.

The same logic extends to combination tricasts. If you’ve boxed a tricast on four horses (24 lines at £1 each, total £24) and one is withdrawn, the lines involving the withdrawn horse are voided and refunded. The remaining live lines are the orderings of the three surviving horses (6 lines, total £6 live stake). If the surviving three fill the trifecta in any order, the matching live line collects the CST dividend at the post-withdrawal SPs.

The Tote treatment – pool recalculation when a horse withdraws

The Tote handles withdrawals through a different mechanic. The pool doesn’t apply a Tattersalls-style deduction. Instead, the pool is recalculated to remove the stake that backed the withdrawn horse. Every unit that included the withdrawn horse in its selections is refunded, the post-takeout pool is reduced accordingly, and the dividend per winning unit is calculated on the smaller pool against the smaller number of surviving winning units.

For boxing purposes, this means a Tote Trifecta on a four-horse box where one horse withdraws works the same arithmetic as the CST equivalent: lines involving the withdrawn horse refund, surviving lines remain live, and the eventual dividend reflects the smaller pool. The 2025 Grand National is one example where a CSF Tricast exceeded the Tote Trifecta on the same finishing order – a reversal that happens in roughly 20% of cases across the calendar and is partly driven by exactly the kind of pool recalculation dynamics that withdrawals can trigger.

The takeout itself doesn’t change. The Tote retains the same percentage of the post-refund pool that it would have retained of the original pool. The effect is purely arithmetic – fewer pounds in the pool, divided among fewer winning units, often producing a per-unit dividend that’s higher than it would have been without the withdrawal if the withdrawn horse was popular and short-priced.

Getting your refund right – what the operator should put back on your card

The mechanical settlement of refunds is the same across all major UK operators, but the time it takes for the refund to appear on your account varies. Online slips typically show the recalculated outlay within minutes of the withdrawal being declared. Racecourse slips need to be presented at the Tote window or the bookmaker’s counter after the race, and the refund is usually processed alongside any winnings or losses.

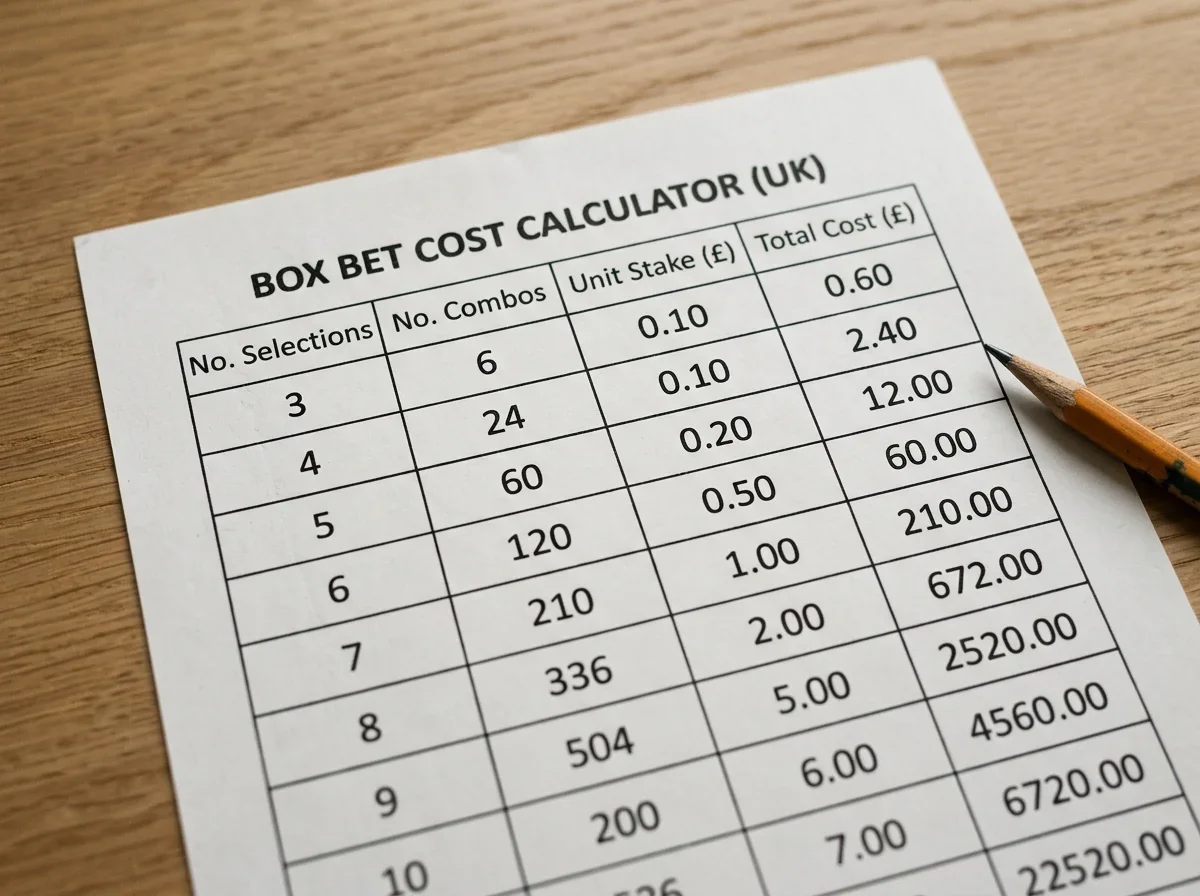

The arithmetic is straightforward when you know what to look for. Take a £1 box trifecta on five horses (120 lines, £120 outlay). One horse withdraws. The surviving four horses produce 4×3×2 = 24 live lines, total live stake £24. Your refund should be £96 – the £120 outlay minus the £24 of stake that’s still live on the race.

The minimum unit stake at most UK operators online is 10p per line, which makes refund accounting more granular but doesn’t change the structure. A 10p box trifecta on six horses costs £12 (120 lines at 10p), and a single withdrawal reduces it to 60 live lines at 10p – a £6 refund and a £6 live stake remaining on the race.

If the refund doesn’t match this arithmetic, push the operator on it. The mechanics are deterministic, and any discrepancy is either a settlement error or a misapplication of the Rule. The same arithmetic governs the cost side I walk through in this guide to box-bet costs across different selection counts, where the unit-stake mechanics are laid out at every common perm size.

Is my combination tricast voided if one of three selected horses doesn’t run?

Not the whole bet – only the lines that include the withdrawn horse. If you’ve boxed three horses (six lines), a single withdrawal voids the four lines involving the withdrawn horse and leaves two live lines on the surviving pair. Those two lines settle against the post-withdrawal SPs as normal.

Does Rule 4 apply to Tote Exacta or only to fixed-odds forecasts?

The Tote doesn’t apply Tattersalls Rule 4 in its named form. The Tote handles withdrawals by refunding units that included the withdrawn horse and recalculating the pool against the remaining stakes. The end effect on dividends can be similar to Rule 4 – a smaller pool divided among fewer winning units – but the mechanism is pool recalculation rather than rule-driven deduction.

Creado por la redacción de «box bet in Horse Racing».